To apply for a home equity loan, you need key documents such as proof of income, including recent pay stubs or tax returns, and documentation of your property's value like a recent appraisal or property tax statement. Lenders also require your credit report and details of any existing mortgages or liens on the home. Having these documents ready streamlines the application process and improves your chances of approval.

What Documents Do You Need for a Home Equity Loan Application?

| Number | Name | Description |

|---|---|---|

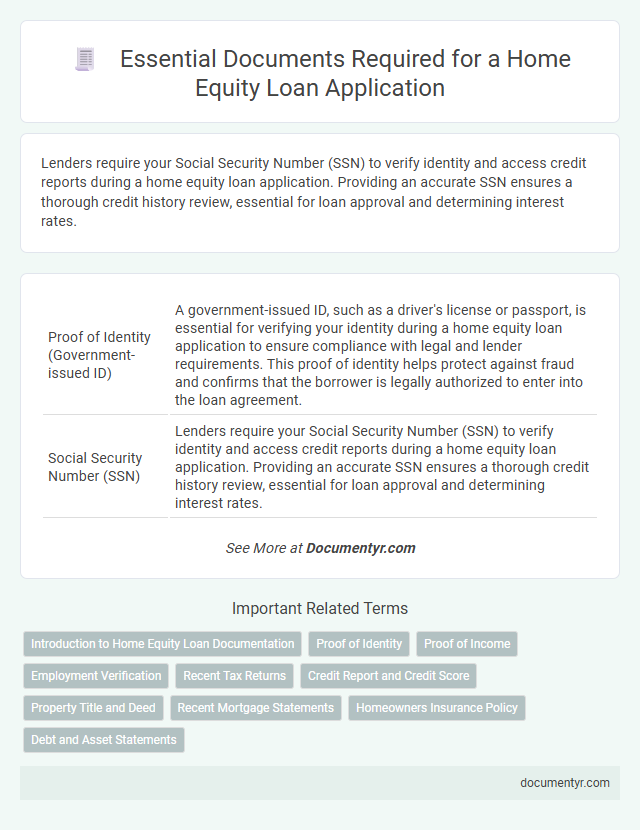

| 1 | Proof of Identity (Government-issued ID) | A government-issued ID, such as a driver's license or passport, is essential for verifying your identity during a home equity loan application to ensure compliance with legal and lender requirements. This proof of identity helps protect against fraud and confirms that the borrower is legally authorized to enter into the loan agreement. |

| 2 | Social Security Number (SSN) | Lenders require your Social Security Number (SSN) to verify identity and access credit reports during a home equity loan application. Providing an accurate SSN ensures a thorough credit history review, essential for loan approval and determining interest rates. |

| 3 | Proof of Income (Pay Stubs) | Pay stubs are essential documents for a home equity loan application as they provide verifiable evidence of the borrower's current income, helping lenders assess repayment ability. Consistent pay stubs showing sufficient salary over recent months significantly enhance approval chances by demonstrating financial stability. |

| 4 | W-2 Forms | W-2 forms are essential for a home equity loan application as they verify your employment income and help lenders assess your repayment ability. Submitting W-2s from the past two years provides a clear financial history and strengthens your loan eligibility. |

| 5 | Tax Returns (Last 2 Years) | Tax returns from the last two years provide lenders with a comprehensive view of your income stability and financial history, essential for assessing your eligibility for a home equity loan. These documents verify reported earnings, help calculate debt-to-income ratios, and confirm your ability to repay the loan. |

| 6 | Bank Statements (Recent Months) | Recent bank statements from the past two to three months are essential for a home equity loan application as they provide lenders with proof of steady income, financial stability, and spending habits. These documents help verify your ability to repay the loan and assess risk by showcasing consistent deposits, bill payments, and overall cash flow. |

| 7 | Mortgage Statement (Current) | A current mortgage statement is essential for a home equity loan application as it provides verified information on the outstanding loan balance, payment history, and remaining term, helping lenders assess your equity and repayment capacity accurately. This document also confirms your property's lien status and supports transparent evaluation of your financial obligations. |

| 8 | Proof of Homeowners Insurance | Proof of homeowners insurance is required for a home equity loan application to ensure the property is protected against damage or loss, safeguarding both the borrower and lender's investment. This document typically includes the insurance policy declaration page outlining coverage limits, policyholder details, and the effective dates of the insurance. |

| 9 | Property Tax Statements | Property tax statements are essential documents for a home equity loan application as they verify the property's assessed value and confirm timely tax payments, which lenders use to evaluate the borrower's financial responsibility. Providing the latest property tax statements ensures accurate collateral appraisal and strengthens the loan approval process. |

| 10 | Credit Report Authorization | A credit report authorization form is essential for a home equity loan application as it grants the lender permission to access your credit history and evaluate your creditworthiness. This document typically includes your personal information and signature, enabling the lender to obtain accurate credit scores and assess the risk profile for loan approval. |

| 11 | Employment Verification Letter | An employment verification letter is a crucial document for a home equity loan application, confirming your current job status, position, salary, and length of employment to lenders. This letter helps verify your income stability and ability to repay the loan, enhancing your approval chances. |

| 12 | Debt Information (Statements of Other Loans) | Debt information for a home equity loan application requires detailed statements of existing loans, including current balances, monthly payments, and lender contact information. Providing accurate documentation on mortgages, auto loans, and credit card debts helps lenders assess your creditworthiness and debt-to-income ratio effectively. |

| 13 | Home Appraisal Report (if required) | A Home Appraisal Report is often required to determine the current market value of your property, ensuring the loan amount aligns with your home's equity. This detailed evaluation, conducted by a certified appraiser, provides lenders with an accurate assessment to mitigate lending risks and finalize the loan approval. |

| 14 | Divorce Decree or Separation Agreement (if applicable) | Provide a Divorce Decree or Separation Agreement to verify your marital status and clarify property and debt responsibilities when applying for a home equity loan. Lenders require this documentation to assess your financial obligations and ensure accurate evaluation of your loan eligibility. |

| 15 | Proof of Additional Assets (IRA, 401k, Investments) | Proof of additional assets such as IRA statements, 401(k) account summaries, and investment portfolio reports are essential for a home equity loan application to demonstrate financial stability and increase borrowing capacity. Lenders require these documents to verify the applicant's net worth and ability to repay the loan, often requesting recent quarterly or annual statements directly from financial institutions. |

Introduction to Home Equity Loan Documentation

Applying for a home equity loan requires submitting specific documents to verify your financial status and property details. These documents help lenders assess your eligibility and determine loan terms.

Key documents typically include proof of income, property appraisal reports, and credit history statements. Proper preparation of these materials streamlines the application process and improves approval chances.

Proof of Identity

What types of proof of identity are required for a home equity loan application? Lenders require valid government-issued identification such as a passport or driver's license to verify your identity. This step ensures security and prevents fraud during the approval process.

Proof of Income

Proof of income is a critical document when applying for a home equity loan. It verifies your ability to repay the loan and supports the lender's risk assessment.

- Pay Stubs - Recent pay stubs demonstrate consistent earnings and employment status.

- Tax Returns - Tax returns from the past two years provide comprehensive income verification, especially for self-employed individuals.

- Bank Statements - Bank statements show income deposits and financial stability over time.

Employment Verification

Employment verification is crucial when applying for a home equity loan to confirm your income stability and job status. Lenders require recent pay stubs, W-2 forms, and sometimes contact details of your employer for direct verification.

Proof of consistent income reassures lenders about your loan repayment ability. Providing accurate employment documents speeds up the home equity loan approval process significantly.

Recent Tax Returns

Recent tax returns are crucial when applying for a home equity loan. Lenders use these documents to verify income and assess financial stability.

Typically, you need to provide your federal tax returns from the past two years. These include W-2 forms, 1099s, and any Schedule C if self-employed. Accurate and complete tax returns help streamline the approval process for the loan.

Credit Report and Credit Score

A credit report provides lenders with a comprehensive history of your borrowing and repayment behavior. A strong credit score is crucial for securing favorable terms on a home equity loan application.

- Credit Report - Details your credit accounts, payment history, and any outstanding debts to assess your financial reliability.

- Credit Score - A numerical representation of your creditworthiness that impacts loan approval and interest rates.

- Document Requirements - Lenders use both credit reports and scores to verify your financial status and determine loan eligibility.

Property Title and Deed

When applying for a home equity loan, the property title and deed are essential documents that verify your ownership of the property. The property title confirms legal ownership while the deed provides detailed information about the property boundaries and transfer history. Lenders require these documents to assess the property's value and ensure there are no liens or encumbrances that could affect the loan.

Recent Mortgage Statements

| Document | Importance | Details |

|---|---|---|

| Recent Mortgage Statements | Essential for verifying current loan status | These statements provide proof of your current mortgage balance, payment history, and lender information. Lenders use this data to assess your existing debt and calculate your available equity. |

| Proof of Income | Supports repayment capacity | Pay stubs, tax returns, and W-2 forms demonstrate your income stability, helping lenders evaluate your ability to repay the loan. |

| Credit Report Authorization | Enables creditworthiness assessment | Allows lenders to review your credit score and history, which impacts eligibility and interest rates for a home equity loan. |

| Property Information | Confirms asset details | Property tax statements or appraisal reports verify the current value of your home, essential for loan-to-value calculations. |

Homeowners Insurance Policy

When applying for a home equity loan, a current homeowners insurance policy is essential to protect the lender's investment. The policy must cover the full replacement cost of the home and be active throughout the loan term. Lenders require proof of insurance to ensure the property is safeguarded against damages that could affect its value.

What Documents Do You Need for a Home Equity Loan Application? Infographic