To claim crypto losses on taxes, you need detailed transaction records, including dates of purchases and sales, amounts, and the value in USD at the time of each transaction. IRS Form 8949, which reports sales and distributions of capital assets, must be completed with this data. Additionally, keep any wallet statements, exchange reports, and proof of cost basis to accurately support your claim.

What Documents are Needed for Claiming Crypto Losses on Taxes?

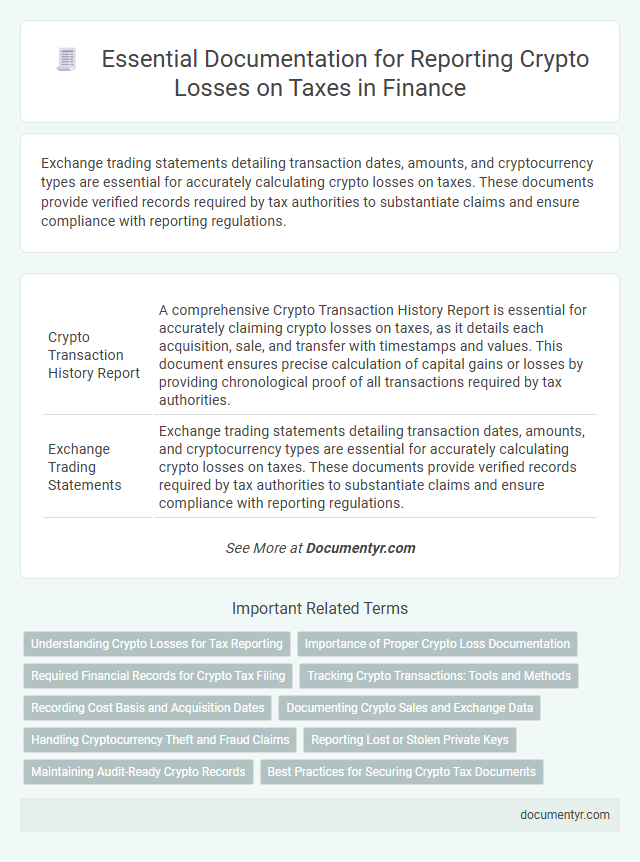

| Number | Name | Description |

|---|---|---|

| 1 | Crypto Transaction History Report | A comprehensive Crypto Transaction History Report is essential for accurately claiming crypto losses on taxes, as it details each acquisition, sale, and transfer with timestamps and values. This document ensures precise calculation of capital gains or losses by providing chronological proof of all transactions required by tax authorities. |

| 2 | Exchange Trading Statements | Exchange trading statements detailing transaction dates, amounts, and cryptocurrency types are essential for accurately calculating crypto losses on taxes. These documents provide verified records required by tax authorities to substantiate claims and ensure compliance with reporting regulations. |

| 3 | Wallet Transaction Logs | Wallet transaction logs serve as essential documentation when claiming crypto losses on taxes, providing a detailed record of all cryptocurrency transfers, purchases, and sales with timestamps and transaction IDs. Accurate logs from wallets help substantiate the cost basis, sale proceeds, and loss amounts required by tax authorities to validate claims and calculate capital gains or losses. |

| 4 | Form 8949 (Sales and Other Dispositions of Capital Assets) | To claim crypto losses on taxes, you must complete Form 8949, which details each transaction's date, proceeds, cost basis, and resulting gain or loss. Accurate records including exchange statements, purchase receipts, and wallet transaction histories are essential for filling out Form 8949 correctly and substantiating your claims with the IRS. |

| 5 | IRS Schedule D (Capital Gains and Losses) | To claim crypto losses on taxes, taxpayers must complete IRS Schedule D, which details capital gains and losses, requiring accurate records of purchase dates, sale dates, cost basis, and proceeds from each transaction. Supporting documents include transaction histories from exchanges, wallet statements, and Form 1099-B if provided, ensuring comprehensive reporting for IRS compliance. |

| 6 | Purchase and Sale Receipts | Purchase and sale receipts are essential documents for claiming crypto losses on taxes as they provide concrete evidence of transaction dates, amounts, and values. These records enable accurate calculation of cost basis, realized losses, and support compliance with IRS reporting requirements. |

| 7 | Cost Basis Documentation | Accurate cost basis documentation is essential for claiming crypto losses on taxes, including detailed records of purchase dates, acquisition prices, transaction fees, and amounts of cryptocurrency acquired. This information allows taxpayers to precisely calculate capital losses by comparing the original investment costs with the sale or disposal proceeds, ensuring compliance with IRS regulations. |

| 8 | Transfer Receipts | Transfer receipts are essential documents for claiming crypto losses on taxes, providing proof of the amount, date, and value of the transferred cryptocurrency. Accurate records of wallet addresses, transaction IDs, and timestamps ensure the correct calculation of gains or losses for tax reporting purposes. |

| 9 | Mining or Staking Earnings Records | Accurate records of mining or staking earnings, including detailed transaction histories, wallet addresses, and the fair market value of the mined or staked cryptocurrency at the time of receipt, are essential for claiming crypto losses on taxes. Documentation such as payout statements from mining pools, staking reward summaries, and any associated expenses like electricity costs or hardware purchases must be maintained to substantiate claims and comply with tax regulations. |

| 10 | Lost/Stolen Crypto Incident Reports | Lost or stolen crypto incident reports serve as critical documentation when claiming crypto losses on taxes, providing a formal record detailing the date, amount, and circumstances of the loss. These reports, alongside transaction histories and wallet data, substantiate claims and ensure compliance with IRS requirements for deducting losses from virtual currency theft or loss. |

| 11 | Communications with Exchanges (regarding losses) | Communications with exchanges, including account statements, transaction histories, and official correspondence detailing loss events, are crucial for accurately documenting crypto losses on tax filings. IRS guidelines emphasize retaining these records to substantiate claims during audits and ensure compliance with tax reporting requirements. |

| 12 | Tax Advisor Correspondence | Tax advisor correspondence is essential for accurately claiming crypto losses on taxes, as it provides professional guidance on necessary documentation such as transaction histories, digital wallet statements, and proof of purchase prices. These detailed records, verified and interpreted by tax professionals, ensure compliance with IRS regulations and maximize eligible deductions. |

| 13 | Supporting Legal Documentation (e.g., theft reports, court filings) | Claiming crypto losses on taxes requires supporting legal documentation such as theft reports and court filings to substantiate the loss with tax authorities. These documents provide essential evidence for IRS Form 8949 and Schedule D, ensuring compliance with tax regulations and maximizing allowable deductions. |

| 14 | Summary of Lost or Inaccessible Funds | A comprehensive summary of lost or inaccessible crypto funds must include transaction records, wallet addresses, and any evidence of theft or technical failure to substantiate losses on tax returns. Detailed documentation, such as blockchain analysis reports and correspondence with exchanges, strengthens claims for accurate tax deduction of crypto losses. |

| 15 | Proof of Ownership (wallet addresses, public keys) | Claiming crypto losses on taxes requires thorough proof of ownership, primarily through wallet addresses and public keys that clearly link you to the digital assets in question. These documents establish the connection between your identity and the cryptocurrency holdings, essential for validating transactions and calculating accurate loss reports to tax authorities. |

Understanding Crypto Losses for Tax Reporting

Claiming crypto losses on taxes requires accurate documentation to support your claims and comply with IRS guidelines. Key documents include transaction histories from exchanges, which detail purchases, sales, and transfers of cryptocurrency.

Understanding crypto losses for tax reporting involves identifying realized losses, which occur when assets are sold below their purchase price. Maintaining detailed records such as wallet addresses, dates of transactions, amounts, and fair market values helps ensure accurate loss calculations.

Importance of Proper Crypto Loss Documentation

Claiming crypto losses on taxes requires thorough documentation to ensure accuracy and compliance with regulations. Proper records help verify your losses and can maximize your tax benefits.

- Transaction History - A detailed record of all cryptocurrency trades, including dates, amounts, and transaction values, is essential for calculating gains and losses.

- Wallet Statements - Statements from digital wallets provide proof of holdings and transfer records necessary for validating ownership and loss claims.

- Cost Basis Records - Documentation of the original purchase price and acquisition dates allows precise determination of loss amounts for tax reporting.

Maintaining organized and complete documentation protects your financial interests and supports accurate tax filing for crypto losses.

Required Financial Records for Crypto Tax Filing

Claiming crypto losses on taxes requires organized financial documentation to accurately report transactions and calculate losses. Proper records support compliance with tax regulations and ensure that all deductible losses are properly accounted for.

- Transaction History - Complete records of all cryptocurrency trades, including dates, amounts, and values at the time of each transaction.

- Purchase and Sale Receipts - Documentation showing the cost basis and sale proceeds of each crypto asset to determine the exact loss or gain.

- Wallet and Exchange Statements - Statements from wallets and exchanges that verify transaction details and holdings for the relevant tax year.

Tracking Crypto Transactions: Tools and Methods

What documents are needed for claiming crypto losses on taxes? Accurate tracking of all crypto transactions is essential for tax reporting. Tools like blockchain explorers, crypto portfolio trackers, and transaction history downloads from exchanges provide critical data.

How can one effectively track crypto transactions for tax purposes? Utilizing specialized software such as CoinTracker, Koinly, or CryptoTrader.Tax simplifies transaction aggregation. These tools help compile purchase dates, amounts, and prices necessary for calculating gains or losses.

What methods improve accuracy in documenting crypto losses? Keeping detailed records including wallet addresses, transaction IDs, and timestamps ensures transparent reporting. Exported CSV files from exchanges serve as verifiable proof when filing taxes.

Recording Cost Basis and Acquisition Dates

When claiming crypto losses on taxes, it is essential to have detailed records of your cost basis and acquisition dates. Accurate documentation ensures correct reporting and maximizes potential tax benefits.

Cost basis records should include the original purchase price of the cryptocurrency, along with transaction fees. Acquisition dates must be clearly documented to determine whether assets are short-term or long-term holdings. These details are fundamental for calculating capital gains or losses accurately on tax returns.

Documenting Crypto Sales and Exchange Data

Claiming crypto losses on taxes requires thorough documentation of all crypto sales and exchanges. Key documents include transaction histories from exchanges showing dates, amounts, and transaction types. Accurate records of cost basis and sale proceeds help support loss claims during tax filing.

Handling Cryptocurrency Theft and Fraud Claims

Claiming crypto losses on taxes requires specific documentation to validate your claim effectively. Essential documents include transaction histories, wallet statements, and theft or fraud reports filed with authorities.

Handling cryptocurrency theft and fraud claims demands proof of unauthorized activity and communication with exchanges or law enforcement. Accurate records of your original investment and dates of theft support the IRS in verifying your reported losses.

Reporting Lost or Stolen Private Keys

Claiming crypto losses on taxes requires thorough documentation, especially when reporting lost or stolen private keys. Key documents include proof of ownership, transaction histories, and official reports filed with authorities to validate the loss. Accurate records help substantiate claims and ensure compliance with IRS guidelines on digital asset losses.

Maintaining Audit-Ready Crypto Records

| Document Type | Description | Purpose for Claiming Crypto Losses |

|---|---|---|

| Transaction History | Comprehensive ledger of all cryptocurrency buys, sells, exchanges, and transfers from wallets and exchanges. | Ensures accurate calculation of cost basis and capital losses or gains, critical for IRS audit verification. |

| Exchange Statements | Official reports from cryptocurrency exchanges detailing transaction dates, amounts, prices, and fees. | Validates transaction details and supports loss claims by providing third-party documentation. |

| Wallet Records | Logs from digital wallets showing wallet addresses, transfers, and balances over time. | Confirms asset ownership and movement, reinforcing the legitimacy of reported losses. |

| Cost Basis Documentation | Proof of original purchase price including fees, timestamps, and acquisition source. | Determines the basis for loss calculation by showing accurate acquisition costs. |

| Disposal Documentation | Records of cryptocurrency sales, exchanges, or disposals, including proceeds and dates. | Tracks disposition events to verify when and how losses were realized for tax reporting. |

| IRS Forms and Attachments | Completed IRS Form 8949 and Schedule D outlining capital gains and losses from crypto transactions. | Official forms required to report cryptocurrency loss claims on tax returns accurately. |

| Audit Trail Files | Organized, chronological digital or printed files consolidating all tax-related crypto records. | Facilitates quick response to IRS inquiries and supports transparent record-keeping standards. |

What Documents are Needed for Claiming Crypto Losses on Taxes? Infographic