Lenders typically require comprehensive financial statements, including profit and loss statements, balance sheets, and cash flow projections to assess a small business's creditworthiness. Personal and business tax returns, along with bank statements, provide proof of income and financial stability. A detailed business plan and legal documents such as business licenses, articles of incorporation, and contracts may also be necessary to support the loan application.

What Documents Are Necessary for Small Business Loan Approvals?

| Number | Name | Description |

|---|---|---|

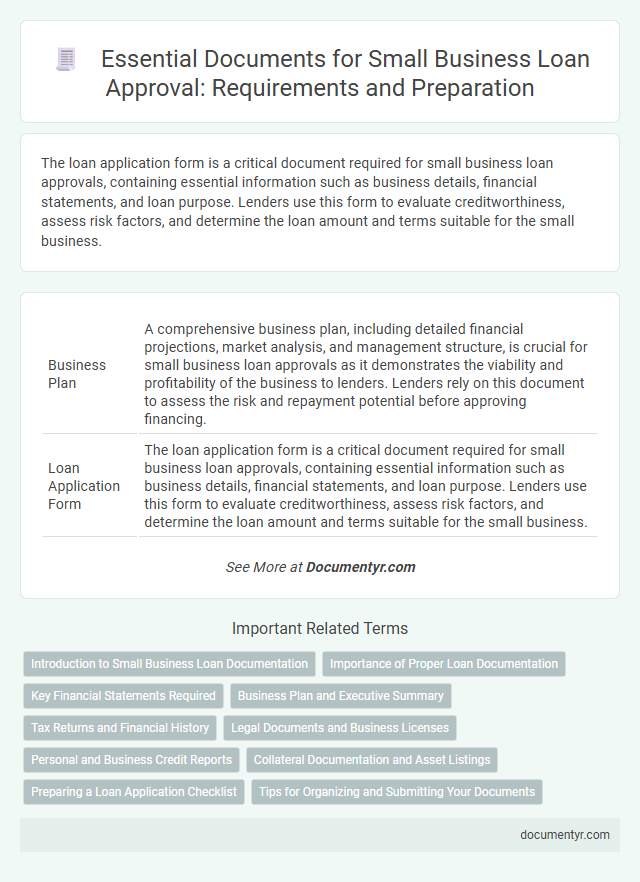

| 1 | Business Plan | A comprehensive business plan, including detailed financial projections, market analysis, and management structure, is crucial for small business loan approvals as it demonstrates the viability and profitability of the business to lenders. Lenders rely on this document to assess the risk and repayment potential before approving financing. |

| 2 | Loan Application Form | The loan application form is a critical document required for small business loan approvals, containing essential information such as business details, financial statements, and loan purpose. Lenders use this form to evaluate creditworthiness, assess risk factors, and determine the loan amount and terms suitable for the small business. |

| 3 | Personal Identification (ID, Passport, Driver's License) | Personal identification documents such as a government-issued ID, passport, or driver's license are essential for verifying the identity of the small business loan applicant, ensuring compliance with lending regulations. Lenders require these forms of identification to confirm the authenticity of the borrower and prevent fraud throughout the loan approval process. |

| 4 | Personal Credit Report | Lenders require a personal credit report to evaluate the borrower's creditworthiness, assessing credit history, outstanding debts, and payment reliability. This document plays a crucial role in small business loan approvals by providing insight into the applicant's financial responsibility and risk level. |

| 5 | Business Credit Report | Lenders require a detailed business credit report that includes credit scores, trade credit history, payment punctuality, and outstanding debts to assess the financial reliability of the small business. This document serves as a critical indicator of creditworthiness and can significantly impact loan approval decisions and interest rates. |

| 6 | Personal Tax Returns (2-3 years) | Lenders require personal tax returns from the past 2-3 years to verify income stability and assess the borrower's financial reliability, which directly impacts small business loan approval decisions. These documents provide detailed insights into individual earnings, deductions, and tax payments, enabling lenders to evaluate creditworthiness comprehensively. |

| 7 | Business Tax Returns (2-3 years) | Business tax returns from the past 2-3 years are essential for small business loan approvals as they provide lenders with verified financial information, demonstrating the business's revenue, expenses, and profitability trends. These documents help assess creditworthiness and the ability to repay the loan, making them a critical part of the loan application process. |

| 8 | Business Bank Statements (6-12 months) | Business bank statements covering 6-12 months are critical for small business loan approvals as they provide lenders with detailed insights into cash flow, revenue consistency, and financial stability. These statements help verify income, track expenses, and assess the borrower's ability to repay the loan, making them essential for accurate credit evaluation. |

| 9 | Balance Sheet | A detailed balance sheet is essential for small business loan approvals as it provides lenders with a snapshot of assets, liabilities, and owner's equity, demonstrating the company's financial stability. Accurate financial statements, including the balance sheet, help lenders assess the business's creditworthiness and repayment capacity. |

| 10 | Income Statement (Profit & Loss Statement) | The Income Statement, also known as the Profit & Loss Statement, is essential for small business loan approvals as it details the company's revenues, expenses, and net profit over a specific period, demonstrating financial health and profitability. Lenders analyze this document to assess cash flow stability, operational efficiency, and the business's ability to repay the loan. |

| 11 | Cash Flow Statement | A detailed cash flow statement is essential for small business loan approvals as it demonstrates the company's ability to generate sufficient cash to meet debt obligations. Lenders rely on this document to assess liquidity, operational efficiency, and the sustainability of cash inflows and outflows over specific periods. |

| 12 | Accounts Receivable Aging Report | Lenders require an Accounts Receivable Aging Report to assess the quality and timeliness of a small business's outstanding invoices, which reflects the company's cash flow health and credit risk. This report categorizes receivables by age, helping lenders evaluate the likelihood of timely payments and the business's ability to repay the loan. |

| 13 | Accounts Payable Aging Report | An Accounts Payable Aging Report is essential for small business loan approvals as it details outstanding debts and payment schedules, demonstrating the company's cash flow management and financial stability to lenders. This report helps identify potential risks by showing timely or overdue payments, influencing the lender's decision to approve the loan. |

| 14 | Business Licenses and Permits | Business licenses and permits are critical documents for small business loan approvals as they verify the legal operation status and ensure compliance with local, state, and federal regulations. Lenders require these documents to assess the legitimacy and risk profile of the business before approving financing. |

| 15 | Articles of Incorporation or Organization | Articles of Incorporation or Organization serve as critical legal documents that verify a small business's formal establishment and corporate structure, essential for loan approval processes. Lenders require these articles to confirm the business's legitimacy, ownership details, and compliance with state regulations before disbursing financing. |

| 16 | Ownership and Affiliation Documents | Ownership and affiliation documents essential for small business loan approvals include articles of incorporation, partnership agreements, business licenses, and ownership certificates that verify legal structure and stakeholder interests. Lenders require these documents to assess business legitimacy, ownership distribution, and related party affiliations, ensuring compliance and risk management. |

| 17 | Commercial Lease Agreement | A commercial lease agreement is a critical document for small business loan approvals as it verifies the business's physical location and operational stability, which lenders assess to mitigate risks. This agreement outlines the lease terms, rent obligations, and duration, providing essential evidence of fixed expenses and a legitimate place of business necessary for underwriting the loan. |

| 18 | Collateral Documentation | Collateral documentation for small business loan approvals must include clear property titles, asset appraisals, and proof of ownership to validate the loan guarantee. Financial institutions often require detailed records such as real estate deeds, equipment inventories, and vehicle registrations to assess the collateral's value and enforceability. |

| 19 | Existing Debt Schedule | An existing debt schedule is essential for small business loan approvals as it provides a detailed list of all current liabilities, including loan balances, payment amounts, interest rates, and maturity dates, helping lenders assess financial health and risk. Accurate and up-to-date debt schedules demonstrate transparency and the borrower's ability to manage cash flow, influencing loan terms and approval likelihood. |

| 20 | Employee Identification Number (EIN) | The Employee Identification Number (EIN) is a critical document required for small business loan approvals, serving as the business's tax identification for verification and credit evaluation. Lenders use the EIN to confirm the legitimacy of the business and streamline the assessment of financial history and tax compliance. |

| 21 | Franchise Agreements (if applicable) | Franchise agreements are crucial for small business loan approvals when the business operates under a franchised model, as they provide lenders with detailed information about the franchise relationship, operational guidelines, and financial obligations. Including a well-documented franchise agreement helps demonstrate business stability and adherence to franchisor standards, increasing lender confidence in loan repayment capability. |

Introduction to Small Business Loan Documentation

Small business loan approvals rely heavily on thorough documentation to assess the borrower's financial stability and creditworthiness. Accurate and complete paperwork streamlines the approval process and increases the chance of funding.

Key documents include financial statements, tax returns, and business plans that demonstrate the company's operational health. Lenders evaluate these papers to minimize risk and ensure repayment capability.

Importance of Proper Loan Documentation

| Document Type | Description | Importance |

|---|---|---|

| Business Plan | A detailed overview of the business, including objectives, strategies, and market analysis. | Helps lenders assess the viability and growth potential of the business. |

| Financial Statements | Includes balance sheets, income statements, and cash flow statements from the past 2-3 years. | Demonstrates the financial health and stability of the business. |

| Tax Returns | Business and personal tax returns for the last 2-3 years. | Verifies income and helps lenders evaluate repayment ability. |

| Bank Statements | Recent bank statements, typically for the last 6-12 months. | Shows cash flow and financial activity within the business. |

| Legal Documents | Business licenses, registrations, and permits relevant to operations. | Confirms the business is legally authorized to operate. |

| Collateral Documentation | Details of assets offered as security for the loan. | Increases lender confidence by providing security for the loan. |

| Personal Identification | Government-issued IDs for business owners or guarantors. | Required for identity verification and creditworthiness checks. |

Proper loan documentation plays a crucial role in small business loan approvals. It provides a clear, organized picture of your business's financial status, operational legitimacy, and repayment capacity. Incomplete or inaccurate documents can lead to delays, rejections, or less favorable loan terms. Ensuring all necessary paperwork is thorough and up to date enhances the chances of securing the funds your business needs.

Key Financial Statements Required

Key financial statements are crucial for small business loan approvals, providing lenders with a clear picture of the business's financial health. Essential documents include the balance sheet, income statement, and cash flow statement, which detail assets, liabilities, revenues, expenses, and cash movements. Your ability to present accurate and up-to-date financial data significantly impacts the lender's decision-making process.

Business Plan and Executive Summary

What key documents are essential for small business loan approvals? A well-prepared business plan is crucial, outlining your company's goals, market analysis, and financial projections. The executive summary provides a concise overview, capturing the lender's attention with your business's value proposition and funding needs.

Tax Returns and Financial History

Tax returns serve as a vital document in small business loan approvals, providing lenders with verified income information and business profitability over time. Detailed financial history complements tax returns by offering insights into cash flow, liabilities, and creditworthiness.

Lenders typically require at least two to three years of both personal and business tax returns to assess consistent revenue streams and financial stability. A comprehensive financial history includes bank statements, profit and loss statements, and balance sheets that reveal the business's operational health. Together, these documents help lenders evaluate risk and make informed lending decisions.

Legal Documents and Business Licenses

Legal documents are crucial for small business loan approvals, serving as proof of your business's legitimacy and financial stability. Key legal documents often include articles of incorporation, partnership agreements, and tax identification numbers.

Business licenses and permits demonstrate compliance with local and state regulations, which lenders require to reduce their lending risks. Providing valid business licenses helps ensure a smoother approval process and builds lender confidence in your business operations.

Personal and Business Credit Reports

Small business loan approvals require comprehensive documentation to evaluate creditworthiness and financial stability. Personal and business credit reports play a crucial role in this assessment process.

- Personal Credit Report - Lenders review personal credit reports to assess the borrower's credit history, payment behavior, and overall financial responsibility.

- Business Credit Report - This report reflects the company's credit activity, including payment history with suppliers and outstanding debts, providing insight into business financial health.

- Credit Report Scores - Both personal and business credit scores influence lender decisions by quantifying risk and predicting the likelihood of loan repayment.

Collateral Documentation and Asset Listings

Collateral documentation and detailed asset listings play a critical role in small business loan approvals, providing lenders with assurance of repayment security. Properly prepared documents demonstrate business stability and asset value, influencing loan terms and approval chances.

- Collateral Documentation - Legal documents verifying ownership and value of assets pledged as loan security.

- Asset Listings - Comprehensive inventory of business assets including equipment, property, and receivables.

- Appraisal Reports - Professional valuations confirming the current market worth of collateral assets.

Submitting accurate and thorough collateral and asset documentation accelerates the loan approval process and enhances lender confidence.

Preparing a Loan Application Checklist

Preparing a loan application checklist is essential for small business loan approvals. Key documents include financial statements, tax returns, and a detailed business plan. Providing accurate documentation increases the likelihood of securing financing efficiently.

What Documents Are Necessary for Small Business Loan Approvals? Infographic