Lenders require key documents for mortgage pre-approval, including proof of income such as recent pay stubs, W-2 forms, and tax returns. Verification of assets like bank statements and investment accounts is necessary to demonstrate financial stability. Borrowers must also provide identification details and credit history to complete the evaluation process efficiently.

What Documents Are Essential for Mortgage Pre-Approval?

| Number | Name | Description |

|---|---|---|

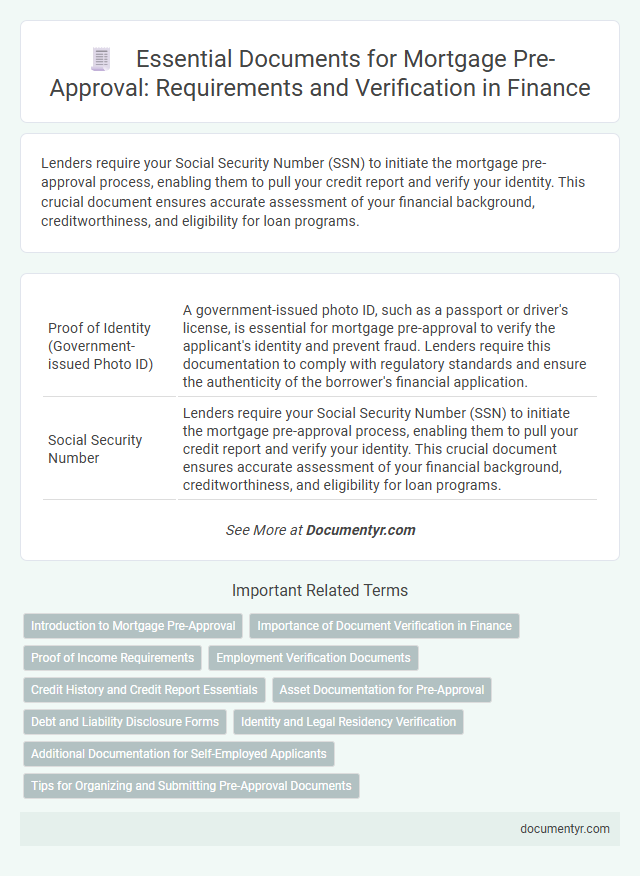

| 1 | Proof of Identity (Government-issued Photo ID) | A government-issued photo ID, such as a passport or driver's license, is essential for mortgage pre-approval to verify the applicant's identity and prevent fraud. Lenders require this documentation to comply with regulatory standards and ensure the authenticity of the borrower's financial application. |

| 2 | Social Security Number | Lenders require your Social Security Number (SSN) to initiate the mortgage pre-approval process, enabling them to pull your credit report and verify your identity. This crucial document ensures accurate assessment of your financial background, creditworthiness, and eligibility for loan programs. |

| 3 | Recent Pay Stubs | Recent pay stubs are essential for mortgage pre-approval as they provide lenders with up-to-date evidence of your current income, verifying your ability to repay the loan. These documents typically cover the most recent 30 days of earnings and help assess stability and consistency in your employment income. |

| 4 | W-2 Forms (Last 2 Years) | W-2 forms from the last two years are crucial for mortgage pre-approval as they verify a borrower's consistent employment income and stability, which lenders rely on to assess the ability to repay the loan. These documents provide detailed information on wages earned and taxes withheld, ensuring accurate income verification during the underwriting process. |

| 5 | Tax Returns (Last 2 Years) | Tax returns from the last two years provide a comprehensive record of your income, helping lenders verify your financial stability and ensure accurate debt-to-income ratio calculations for mortgage pre-approval. These documents include W-2s, 1099s, and other relevant income reports that confirm consistent earnings and identify any potential red flags in your financial history. |

| 6 | Bank Statements (Last 2–3 Months) | Bank statements from the last 2-3 months are crucial for mortgage pre-approval as they verify your income, spending habits, and saving patterns, providing lenders with a clear picture of your financial stability. These documents help confirm consistent deposits and assess your ability to manage monthly mortgage payments, increasing the accuracy of your loan eligibility evaluation. |

| 7 | Proof of Additional Income (e.g., bonuses, alimony) | Proof of additional income, such as bonuses and alimony, requires recent pay stubs, court orders, or legal agreements verifying consistent payments over time. Lenders may also request tax returns or bank statements to confirm the stability and receipt of these supplemental income sources. |

| 8 | Employment Verification Letter | An employment verification letter is crucial for mortgage pre-approval as it confirms the borrower's current job status, income, and length of employment, providing lenders with reliable financial stability evidence. This document typically includes the employer's contact information, job title, salary details, and employment duration, ensuring mortgage underwriters can accurately assess the applicant's ability to repay the loan. |

| 9 | Asset Statements (Retirement, Investments) | Asset statements, including detailed reports of retirement accounts and investment portfolios, are essential for mortgage pre-approval as they demonstrate financial stability and the ability to cover down payments or reserves. Lenders require recent, comprehensive documentation such as 401(k), IRA statements, and brokerage account summaries to accurately assess an applicant's net worth and repayment capacity. |

| 10 | Debt Information (Credit Card, Loan Statements) | Debt information such as credit card statements and loan statements provides lenders with a clear view of an applicant's existing financial obligations and outstanding balances, which are crucial for assessing creditworthiness during mortgage pre-approval. Accurate documentation of current debts helps determine the debt-to-income ratio, a key metric that influences the loan amount and interest rate approval. |

| 11 | Credit Report Authorization | Credit report authorization is essential for mortgage pre-approval, allowing lenders to evaluate your creditworthiness and assess risk accurately. This document grants permission to access your credit history, which directly influences loan terms and approval decisions. |

| 12 | Rental History/Lease Agreements (if applicable) | Rental history and lease agreements provide critical proof of consistent payment behavior and housing stability, which lenders assess during mortgage pre-approval. Submitting at least 12 months of documented rental payments and current lease contracts strengthens your financial reliability in the eyes of mortgage underwriters. |

| 13 | Gift Letter (if using gifted funds for down payment) | A Gift Letter is essential for mortgage pre-approval when using gifted funds for the down payment, as it verifies the money's source and confirms it is a non-repayable gift. This document must detail the donor's information, relationship to the borrower, and declaration that repayment is not expected, ensuring compliance with lender requirements. |

| 14 | Divorce Decree (if applicable) | A Divorce Decree is essential for mortgage pre-approval when marital status affects financial obligations or asset ownership, providing clear evidence of property division, alimony, or child support responsibilities. Lenders require this document to accurately assess your debt-to-income ratio and ensure all financial liabilities are accounted for in the mortgage evaluation. |

| 15 | Bankruptcy/Discharge Papers (if applicable) | Bankruptcy or discharge papers are crucial for mortgage pre-approval as they provide lenders with detailed information about your financial history and the resolution of past debts. These documents help assess your creditworthiness by verifying the status and timing of any bankruptcy filings, influencing loan terms and approval chances. |

Introduction to Mortgage Pre-Approval

| Introduction to Mortgage Pre-Approval | |

|---|---|

| Mortgage pre-approval is a critical first step in the home-buying process. It provides potential borrowers with a clear understanding of their borrowing capacity based on a lender's preliminary evaluation of their financial profile. Pre-approval strengthens a buyer's position by demonstrating seriousness and financial readiness to sellers. This process typically requires submitting specific financial documents to verify income, assets, debts, and creditworthiness. | |

| Essential Documents for Mortgage Pre-Approval | Purpose |

| Proof of Income | Validates employment status and income level through recent pay stubs, W-2 forms, or tax returns |

| Credit Report Authorization | Allows lenders to assess credit history and credit score as part of the risk evaluation |

| Bank Statements | Demonstrates the availability of funds for down payment and closing costs |

| Identification | Verifies borrower identity with government-issued photo IDs like a driver's license or passport |

| Debt Documentation | Includes information on outstanding loans, credit card balances, and other liabilities affecting debt-to-income ratio |

Importance of Document Verification in Finance

Mortgage pre-approval requires submitting key documents that verify your financial status to lenders. Essential documents include proof of income, credit reports, and identification.

The accuracy and authenticity of these documents help lenders assess your creditworthiness effectively. Proper document verification minimizes the risk of loan denial and ensures smooth approval processes.

Proof of Income Requirements

Proof of income is a critical component of mortgage pre-approval to verify the borrower's financial stability and repayment ability. Lenders typically require recent pay stubs, W-2 forms, and tax returns to assess consistent income sources.

Self-employed applicants must provide profit and loss statements along with personal and business tax returns. These documents enable lenders to evaluate income reliability and determine the borrowing capacity accurately.

Employment Verification Documents

Employment verification documents play a crucial role in the mortgage pre-approval process by confirming your income stability. Lenders require these documents to assess your ability to repay the loan reliably.

- Recent Pay Stubs - These provide proof of your current earnings and employment status over the past month or two.

- Employer Contact Information - Lenders may contact your employer directly to verify your job position and salary details.

- Employment Verification Letter - A formal letter from your employer confirming your job title, length of employment, and salary specifics.

Credit History and Credit Report Essentials

Credit history plays a crucial role in mortgage pre-approval by showing lenders your past borrowing and repayment behavior. A detailed credit report, which includes credit scores, outstanding debts, and payment history, is essential for evaluating your financial reliability. Lenders use this information to assess risk and determine your eligibility for a mortgage loan.

Asset Documentation for Pre-Approval

Asset documentation is a critical component of your mortgage pre-approval process. Lenders require detailed records of your financial assets to assess your borrowing capacity accurately.

Essential asset documents include recent bank statements, retirement account statements, and investment portfolio summaries. These documents demonstrate your financial stability and ability to cover down payments and closing costs. Accurate asset documentation helps streamline the mortgage approval process and increases your chances of securing favorable loan terms.

Debt and Liability Disclosure Forms

What role do Debt and Liability Disclosure Forms play in mortgage pre-approval? These documents provide lenders with a comprehensive overview of your outstanding debts and financial obligations. Accurate disclosure helps ensure a realistic assessment of your borrowing capacity.

Identity and Legal Residency Verification

Mortgage pre-approval requires specific documents to verify the applicant's identity and legal residency. Lenders use these documents to ensure compliance with legal and financial regulations during the loan process.

- Government-Issued Photo ID - A valid passport or driver's license confirms the borrower's identity and age.

- Social Security Number or Tax Identification Number - Essential for credit checks and income verification during pre-approval.

- Proof of Legal Residency - Documents such as a visa, green card, or permanent resident card validate the applicant's legal status in the country.

Additional Documentation for Self-Employed Applicants

Mortgage pre-approval requires standard documents such as proof of income, credit report, and employment verification. Self-employed applicants must provide additional documentation, including tax returns from the past two years, profit and loss statements, and business licenses. These documents help lenders assess your financial stability and ability to repay the loan.

What Documents Are Essential for Mortgage Pre-Approval? Infographic