When filing a homeowner's insurance claim, it is essential to provide specific documents to support your case. Common required documents include a completed claim form, proof of homeownership such as a deed or mortgage statement, detailed photographs of the damage, and an inventory of damaged or lost items with their estimated value. Providing receipts, repair estimates, and correspondence with your insurance company can further strengthen your claim and expedite the process.

What Documents are Required for a Homeowner’s Insurance Claim?

| Number | Name | Description |

|---|---|---|

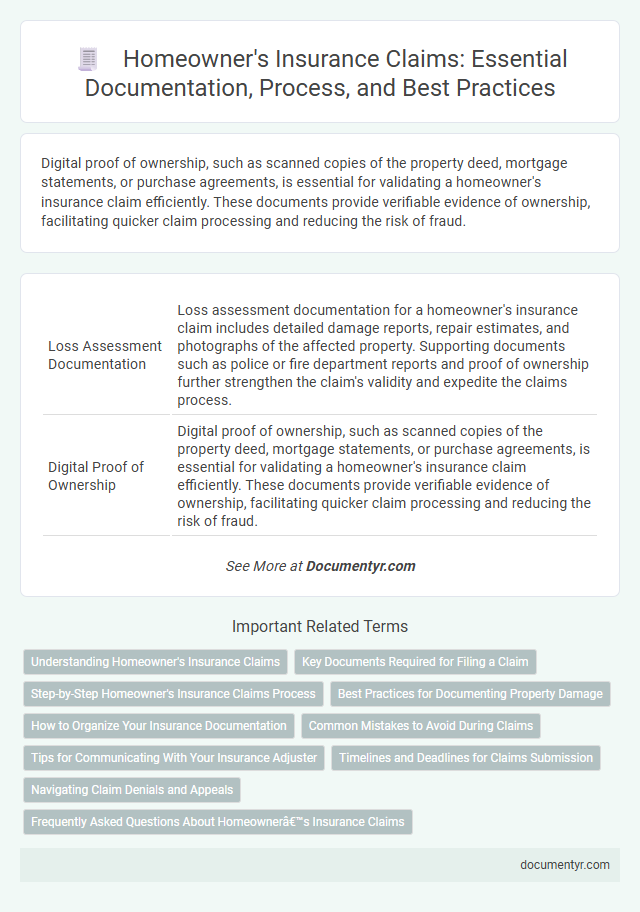

| 1 | Loss Assessment Documentation | Loss assessment documentation for a homeowner's insurance claim includes detailed damage reports, repair estimates, and photographs of the affected property. Supporting documents such as police or fire department reports and proof of ownership further strengthen the claim's validity and expedite the claims process. |

| 2 | Digital Proof of Ownership | Digital proof of ownership, such as scanned copies of the property deed, mortgage statements, or purchase agreements, is essential for validating a homeowner's insurance claim efficiently. These documents provide verifiable evidence of ownership, facilitating quicker claim processing and reducing the risk of fraud. |

| 3 | Restoration Estimate Reports | Restoration estimate reports provide detailed cost assessments for repairing property damage, serving as crucial evidence in homeowner's insurance claims to validate repair expenses. These reports typically include itemized lists of damages, material costs, labor charges, and timeframes for restoration, enabling insurers to accurately process and approve claims. |

| 4 | Smart Home Device Data Logs | Smart home device data logs, such as security camera footage, thermostat records, and smoke detector alerts, provide crucial evidence during a homeowner's insurance claim by verifying the timing and cause of damage. Submitting these digital records alongside traditional documents--like repair estimates, police reports, and photos--enhances claim accuracy and speeds up the approval process. |

| 5 | Drone Imagery Evidence | Drone imagery evidence for a homeowner's insurance claim typically requires high-resolution aerial photos and videos that clearly document property damage, along with metadata verifying the date and location of the footage. Insurers often request supplementary documents such as the drone operator's license, flight log records, and a detailed damage assessment report to validate and expedite the claim process. |

| 6 | Blockchain-Verified Receipts | Blockchain-verified receipts provide tamper-proof evidence of property ownership and purchase details, streamlining the verification process in a homeowner's insurance claim. These digitized documents enhance transparency and reduce fraud risk by securely recording transaction history on an immutable ledger accessible to insurers and homeowners. |

| 7 | Temporary Housing Expense Receipts | Temporary housing expense receipts are essential documents for validating claims related to additional living costs incurred due to property damage. These receipts must clearly detail expenses such as hotel stays, rental accommodations, and meals directly connected to the displacement period, ensuring accurate reimbursement under the homeowner's insurance policy. |

| 8 | Home Inventory App Exports | Home Inventory App Exports provide detailed records of personal belongings, including descriptions, purchase dates, and values, essential for substantiating a homeowner's insurance claim. These digital documents streamline the claims process by offering accurate and organized proof of possessions, reducing delays and disputes. |

| 9 | Sustainability Certification Documents | Sustainability certification documents, such as LEED or Energy Star certifications, are crucial for a homeowner's insurance claim as they verify the eco-friendly features and energy-efficient upgrades of the property. Providing these documents helps insurers assess the true value and sustainability of the home, potentially influencing claim settlements and premium adjustments. |

| 10 | E-Signature Claim Authorizations | E-signature claim authorizations expedite the homeowner's insurance claim process by allowing policyholders to digitally sign and submit necessary documents securely, ensuring faster verification and approval. These electronic documents must include the signed claim form, proof of loss, and authorization to release information, all of which streamline communication between the insurer and the claimant. |

Understanding Homeowner's Insurance Claims

Understanding homeowner's insurance claims requires gathering specific documents to ensure a smooth process. Key documents include the original insurance policy, proof of ownership such as a deed, and detailed photographs or videos of the property damage. Receipts for repairs or replacements, a police or fire report if applicable, and any correspondence with the insurance company further support the claim's validation.

Key Documents Required for Filing a Claim

Filing a homeowner's insurance claim requires specific documents to ensure smooth processing. Key documents include the completed claim form and a copy of the original insurance policy.

Proof of property ownership is essential, such as a deed or mortgage statement. Additionally, submit detailed photographs of the damage and any repair estimates to support the claim.

Step-by-Step Homeowner's Insurance Claims Process

To file a homeowner's insurance claim, gather essential documents such as the insurance policy, proof of loss, and photos or videos of the property damage. Detailed receipts and repair estimates from licensed contractors are crucial to support your claim. Submit all documentation promptly to ensure a smooth step-by-step homeowner's insurance claims process.

Best Practices for Documenting Property Damage

Proper documentation is essential when filing a homeowner's insurance claim to ensure a smooth and efficient process. Detailed records of property damage increase the likelihood of a successful claim settlement.

- Photographic Evidence - Capture clear, timestamped photos of all damaged areas immediately after the incident to provide visual proof.

- Detailed Inventory - Create a comprehensive list of damaged items and property features, including descriptions, quantities, and estimated values.

- Repair and Estimate Reports - Obtain written assessments and cost estimates from licensed contractors or repair professionals to validate the extent of damage.

How to Organize Your Insurance Documentation

Organizing your homeowner's insurance documentation is essential for a smooth claims process. Proper preparation ensures faster claim approval and reduces stress during emergencies.

- Gather All Relevant Documents - Collect your insurance policy, proof of purchase, repair estimates, and photographs of the damage in one place.

- Create Digital Copies - Scan or photograph important documents and store them securely online for easy access anytime.

- Use a Dedicated Folder or Binder - Keep physical copies organized by claim type and date to streamline the submission process.

Maintaining an orderly system for your insurance paperwork accelerates claim handling and improves communication with your insurer.

Common Mistakes to Avoid During Claims

Filing a homeowner's insurance claim requires specific documents to ensure a smooth process. Avoid common mistakes that can delay your claim approval or lead to denial.

- Incomplete Documentation - Submitting missing or partial paperwork like proof of ownership or damage estimates can result in claim delays.

- Poorly Organized Evidence - Disorganized photos, receipts, and repair bills make it difficult for insurers to validate the claim promptly.

- Failure to Report Timely - Delaying the submission of required documents reduces the chance of full claim reimbursement.

Tips for Communicating With Your Insurance Adjuster

What documents are required for a homeowner's insurance claim to ensure a smooth process? Gather the insurance policy, proof of ownership, photos of the damage, repair estimates, and receipts for temporary repairs. Having organized and complete documentation helps facilitate clear communication with your insurance adjuster.

How can you effectively communicate with your insurance adjuster during the claims process? Keep detailed notes of all conversations and promptly provide requested documents. Clear, polite, and timely communication can speed up claim resolution and prevent misunderstandings.

Timelines and Deadlines for Claims Submission

| Document Type | Description | Submission Timeline | Importance |

|---|---|---|---|

| Insurance Policy | Proof of coverage outlining terms and conditions | At claim initiation | Verifies coverage validity and claim eligibility |

| Claim Form | Official document detailing incident and damage | Within 30 days of incident | Essential for processing and record keeping |

| Proof of Loss | Detailed list and description of damaged or lost property | Typically within 60 days of incident | Supports the claim's financial evaluation |

| Photographic Evidence | Images showing extent of damage | As soon as possible after the incident | Helps assessors verify claims and damage scope |

| Repair Estimates or Invoices | Documents from contractors or service providers | Within 60 days or as requested | Used to determine claim payout amounts |

| Police or Incident Reports | Official reports for theft, fire, or other covered events | Immediately or within 24-48 hours | Establishes event authenticity and supports claim validity |

| Deadlines | Varies by insurer and policy; generally 30 to 60 days | Strict adherence required to avoid claim denial | Timely submission ensures claim eligibility and processing |

Navigating Claim Denials and Appeals

When filing a homeowner's insurance claim, you must gather essential documents such as the original insurance policy, proof of loss, repair estimates, and photographic evidence of the damage. Detailed records including receipts for temporary repairs and correspondence with your insurer strengthen your claim.

In case of a claim denial, reviewing the denial letter is crucial to understand the insurer's reasons. Preparing a formal appeal with supporting documents, such as expert assessments or additional photos, improves your chances of reversing the decision.

What Documents are Required for a Homeowner’s Insurance Claim? Infographic