Homeowners must provide key documents such as the property deed, a recent home appraisal, and proof of identity for insurance underwriting. Detailed information about the home's construction, including age, materials used, and any safety features, is also required to assess risk accurately. Providing past insurance records and any claims history helps underwriters determine the appropriate coverage and premium.

What Documents Does a Homeowner Need for Insurance Underwriting?

| Number | Name | Description |

|---|---|---|

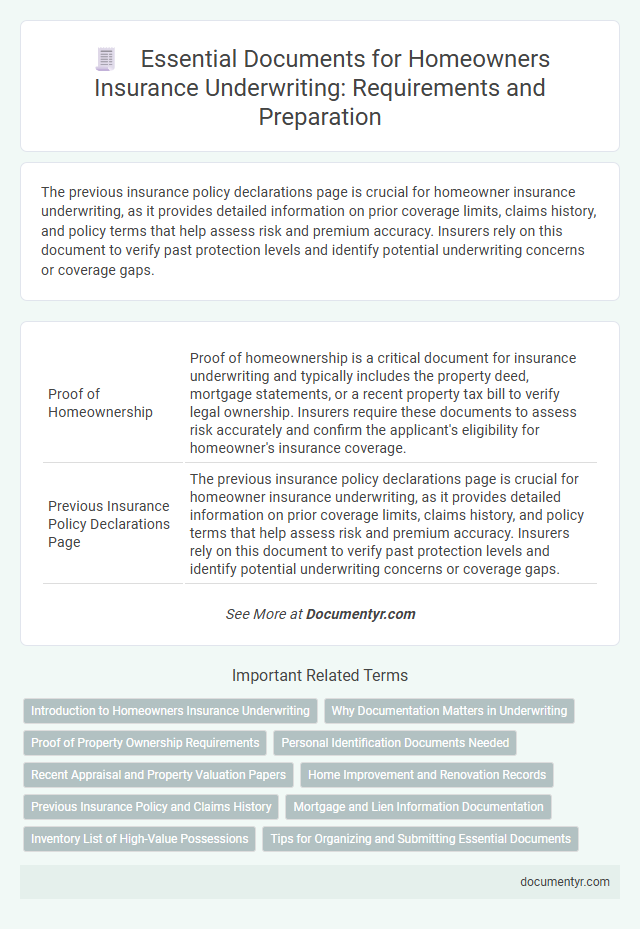

| 1 | Proof of Homeownership | Proof of homeownership is a critical document for insurance underwriting and typically includes the property deed, mortgage statements, or a recent property tax bill to verify legal ownership. Insurers require these documents to assess risk accurately and confirm the applicant's eligibility for homeowner's insurance coverage. |

| 2 | Previous Insurance Policy Declarations Page | The previous insurance policy declarations page is crucial for homeowner insurance underwriting, as it provides detailed information on prior coverage limits, claims history, and policy terms that help assess risk and premium accuracy. Insurers rely on this document to verify past protection levels and identify potential underwriting concerns or coverage gaps. |

| 3 | Mortgage Statement | A mortgage statement is a critical document for insurance underwriting as it verifies the outstanding loan balance, property value, and lender information, which help assess the homeowner's financial obligation and risk profile. Insurers use the mortgage statement to ensure coverage aligns with the property's insured value and mortgage requirements. |

| 4 | Property Deed | A property deed is a crucial document for homeowner insurance underwriting as it verifies ownership and legal description of the property, enabling accurate risk assessment. Insurers use the deed to confirm the property's boundaries, zoning, and any liens that may affect coverage eligibility and premium calculation. |

| 5 | Home Appraisal Report | A Home Appraisal Report is a crucial document for insurance underwriting, providing an expert evaluation of the property's market value and condition. This report helps insurers accurately assess risk and determine appropriate coverage limits for the homeowner's insurance policy. |

| 6 | Recent Home Inspection Report | A recent home inspection report is crucial for insurance underwriting as it provides detailed information on the property's condition, including structural integrity, electrical and plumbing systems, and potential risks like mold or pest infestations. This document helps insurers accurately assess liability and determine appropriate coverage and premiums for the homeowner. |

| 7 | Purchase/Sales Agreement | The Purchase/Sales Agreement is a critical document for insurance underwriting, providing proof of property ownership and detailed information about the transaction including the purchase price and property condition. Insurers use this agreement to assess risk factors and verify the accuracy of the coverage requested, ensuring appropriate premium calculation. |

| 8 | Photo Documentation of Property | Photo documentation of the property is essential for insurance underwriting, providing visual evidence of the home's condition, structural features, and any existing damages or renovations. Clear, date-stamped images of the exterior, interior, roof, foundation, and safety systems help underwriters accurately assess risk and determine appropriate coverage and premiums. |

| 9 | Renovation or Repair Receipts | Renovation or repair receipts are essential documents for insurance underwriting as they provide proof of recent improvements and demonstrate the current condition and value of the property. These receipts help insurers assess risk accurately and determine appropriate coverage and premiums based on updated home features and materials. |

| 10 | Property Tax Statement | A property tax statement is a critical document for homeowner insurance underwriting, providing verified information about the property's assessed value and location. Insurance companies use this statement to accurately assess risk and determine appropriate premium rates based on local tax assessments and property characteristics. |

| 11 | Flood Zone Determination Certificate | A Flood Zone Determination Certificate is essential for homeowners during insurance underwriting to assess flood risk accurately and determine necessary flood insurance requirements. This certificate provides detailed information on whether the property is located within a flood hazard area, influencing premium rates and coverage eligibility. |

| 12 | Building Permits | Building permits are essential documents required for insurance underwriting as they verify that any construction or renovation complies with local regulations and safety standards. Insurers use these permits to assess the risk and ensure the property's structural integrity before approving coverage. |

| 13 | HOA (Homeowners Association) Agreement | A Homeowners Association (HOA) agreement is a critical document for insurance underwriting as it outlines community rules, property maintenance responsibilities, and shared amenities which impact risk assessment. Insurers require the HOA agreement to evaluate coverage needs, liability exposures, and potential claims related to common areas and structural elements governed by the association. |

| 14 | Personal Property Inventory List | A detailed Personal Property Inventory List is essential for homeowners during insurance underwriting, as it provides a comprehensive record of valuable belongings, including descriptions, purchase dates, and estimated values. This document helps insurers accurately assess coverage needs and determine appropriate premium rates based on the homeowner's assets. |

| 15 | Security System Documentation | Homeowners must provide detailed security system documentation, including installation certificates, maintenance records, and proof of active monitoring services, to support insurance underwriting. Insurers evaluate this information to assess risk reduction measures and potentially qualify for premium discounts. |

| 16 | Occupancy Certificate | An Occupancy Certificate is a crucial document for homeowner insurance underwriting as it verifies that the property complies with local building codes and is safe for habitation, reducing insurer risk. Insurers require this certificate to confirm the home's legal occupancy status, ensuring eligibility for coverage and accurate risk assessment. |

| 17 | Proof of Identity | Proof of identity documents required for homeowner insurance underwriting typically include a government-issued ID such as a driver's license or passport, verifying the applicant's legal name and date of birth. Insurers may also request Social Security numbers or tax identification to verify identity and prevent fraud during the underwriting process. |

| 18 | Utility Bills (for address confirmation) | Utility bills, such as electricity, water, or gas statements, serve as essential proof of address during the insurance underwriting process, verifying the homeowner's residence location. Insurers rely on these documents to confirm the property's address, ensuring accurate risk assessment and policy issuance. |

| 19 | Fire Safety Compliance Certificate | A Fire Safety Compliance Certificate is essential for homeowner insurance underwriting, as it verifies that the property meets local fire safety regulations and reduces the insurer's risk exposure. Providing this certificate helps streamline the underwriting process and may lead to more favorable insurance premiums. |

| 20 | Liability Waivers (if applicable) | Liability waivers, when applicable, serve as critical documents in homeowner insurance underwriting by outlining the transfer or limitation of liability between parties, helping insurers assess risk exposure. Providing clear and legally binding liability waivers can expedite the underwriting process and potentially lower premium costs by minimizing uncertain liabilities. |

Introduction to Homeowners Insurance Underwriting

Homeowners insurance underwriting involves assessing the risk associated with insuring a property. This process determines policy eligibility and premium rates based on detailed information about the home and the homeowner.

Key documents required for underwriting include the property deed, recent home inspection reports, and proof of prior insurance coverage. Insurers also request detailed information about the home's construction, age, and safety features. Accurate documentation helps underwriters evaluate potential risks to ensure appropriate coverage and pricing.

Why Documentation Matters in Underwriting

Accurate documentation is essential for homeowner insurance underwriting because it verifies the property's condition, ownership, and value. Insurers rely on these documents to assess risk and determine appropriate coverage and premiums.

Providing detailed records helps prevent delays and potential claim disputes, ensuring a smoother underwriting process. Clear evidence of property details and past maintenance supports more accurate risk evaluation by underwriters.

Proof of Property Ownership Requirements

Proof of property ownership is a crucial document required for insurance underwriting. It verifies your legal right to the insured home and protects against fraudulent claims.

Common documents include a deed, mortgage statement, or property tax bill. These documents confirm ownership details and help underwriters assess risk accurately.

Personal Identification Documents Needed

Homeowners need to provide valid personal identification documents for insurance underwriting, such as a government-issued photo ID like a driver's license or passport. Proof of residence, including utility bills or lease agreements, may also be required to verify homeownership status. These documents help insurers accurately assess risk and confirm the identity of the policy applicant.

Recent Appraisal and Property Valuation Papers

| Document Type | Description | Importance for Insurance Underwriting |

|---|---|---|

| Recent Appraisal Report | Detailed assessment of the property's current market value conducted by a certified appraiser. | Provides accurate valuation data to determine coverage limits and premium rates accurately. |

| Property Valuation Papers | Official documents including comparative market analysis, property tax assessments, and prior appraisals. | Supports verification of property worth, ensuring underwriting aligns with real market conditions. |

| Property Deeds and Titles | Proof of ownership and legal description of the home. | Confirms your rights over the property and assists in risk evaluation by the insurer. |

| Repair and Renovation Records | Documentation of any recent upgrades or structural changes. | Helps underwriters assess increased value or potential hazards affecting the property. |

Home Improvement and Renovation Records

Home improvement and renovation records are essential documents for insurance underwriting as they provide detailed information about the property's condition and upgrades. These records help insurers assess risk and determine appropriate coverage and premiums.

- Detailed Receipts - Includes invoices and proof of payment for materials and labor to verify the scope and quality of renovations.

- Permits and Approvals - Official permits from local authorities confirm that renovations comply with building codes and safety regulations.

- Contractor Information - Documents listing licensed contractors and their work scope ensure renovations were performed professionally and meet industry standards.

Previous Insurance Policy and Claims History

Providing a previous insurance policy and claims history is crucial for homeowner insurance underwriting. These documents help insurers assess risk and determine accurate premium rates.

- Previous Insurance Policy - Shows coverage details and policy duration, helping underwriters verify continuous protection and prior risk assessments.

- Claims History - Reveals the frequency and severity of past claims, indicating potential risk factors for future claims.

- Claims Documentation - Includes paid or denied claim records, assisting in evaluating the homeowner's loss experience and insurance behavior.

Submitting complete and accurate previous insurance records expedites the underwriting process and supports fair premium calculation.

Mortgage and Lien Information Documentation

Mortgage and lien information documentation is critical for insurance underwriting as it verifies ownership and outstanding obligations on the property. Proper documentation ensures accurate risk assessment and policy issuance.

- Mortgage Statement - Provides the current balance, lender details, and payment status for the home loan.

- Deed of Trust - Establishes the legal agreement securing the mortgage lien on the property.

- Lien Release Documents - Confirms that previous liens have been satisfied and removed from the title.

Inventory List of High-Value Possessions

An inventory list of high-value possessions is essential for homeowner insurance underwriting to accurately assess coverage needs. Detailed documentation, including descriptions, purchase receipts, and appraisals, helps establish the value of items like jewelry, electronics, and artwork. Ensuring Your list is thorough can prevent coverage gaps and streamline the claims process.

What Documents Does a Homeowner Need for Insurance Underwriting? Infographic