Flood insurance underwriting requires several documents to accurately assess risk and coverage needs. Key documents include a detailed property elevation certificate, a current flood zone determination, and proof of property ownership. Insurers may also request prior flood loss history and any relevant mitigation measures or improvements to reduce flood risk.

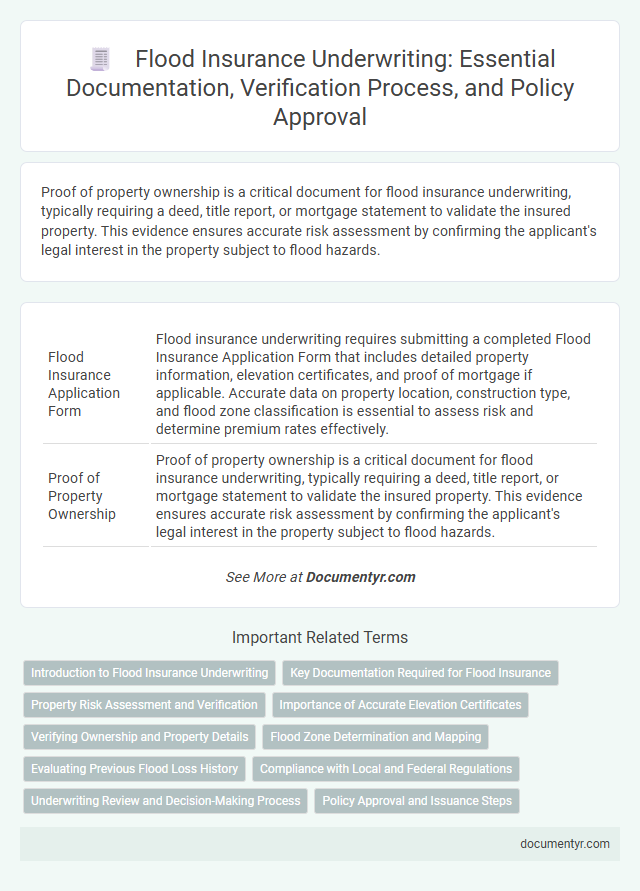

What Documents are Needed for Flood Insurance Underwriting?

| Number | Name | Description |

|---|---|---|

| 1 | Flood Insurance Application Form | Flood insurance underwriting requires submitting a completed Flood Insurance Application Form that includes detailed property information, elevation certificates, and proof of mortgage if applicable. Accurate data on property location, construction type, and flood zone classification is essential to assess risk and determine premium rates effectively. |

| 2 | Proof of Property Ownership | Proof of property ownership is a critical document for flood insurance underwriting, typically requiring a deed, title report, or mortgage statement to validate the insured property. This evidence ensures accurate risk assessment by confirming the applicant's legal interest in the property subject to flood hazards. |

| 3 | Property Deed or Title | A clear and verifiable property deed or title is essential for flood insurance underwriting as it establishes ownership and legal boundaries of the insured property. This document helps insurers assess risk accurately by confirming the property's location relative to flood zones and ensuring that the applicant has the right to insure the property. |

| 4 | Elevation Certificate | An Elevation Certificate is a critical document for flood insurance underwriting, providing detailed information about a building's elevation relative to the base flood elevation (BFE) to accurately assess flood risk. Insurance companies rely on this certificate to determine premium rates and eligibility for National Flood Insurance Program (NFIP) policies. |

| 5 | Flood Zone Determination | Flood insurance underwriting requires precise flood zone determination based on FEMA flood maps, property elevation certificates, and detailed site location information. Accurate assessment of these documents ensures proper risk evaluation and premium calculation. |

| 6 | Prior Insurance Policies | For flood insurance underwriting, prior insurance policies such as previous flood insurance declarations and loss history reports are crucial to assess risk accurately. Providing documentation of claims made under past flood policies helps underwriters evaluate potential exposure and set appropriate premiums. |

| 7 | Property Appraisal Report | A detailed Property Appraisal Report is essential for flood insurance underwriting, providing a comprehensive evaluation of the property's structure, elevation, and overall condition to assess flood risk accurately. This report, often prepared by a certified appraiser, includes critical data such as flood zone designation, foundation type, and proximity to water bodies, which influence premium calculations and coverage terms. |

| 8 | Photographs of Property (Interior/Exterior) | Photographs of the property, both interior and exterior, are essential for flood insurance underwriting as they provide visual evidence of the building's condition, materials, and elevation relative to flood risk. Insurers use these images to assess potential vulnerabilities and verify compliance with floodplain management regulations. |

| 9 | Proof of Address | Flood insurance underwriting requires proof of address documents such as utility bills, lease agreements, or government-issued identification that confirm the insured property's location within a flood zone. Accurate address verification ensures proper risk assessment and compliance with FEMA flood insurance guidelines. |

| 10 | Lease Agreement (if applicable) | A lease agreement is essential for flood insurance underwriting when the insured property is leased, as it verifies occupancy and responsibility for flood risk coverage. This document helps underwriters assess liability and ensures appropriate flood insurance limits are applied based on tenant or owner roles. |

| 11 | Mortgage Statement | A mortgage statement is a critical document for flood insurance underwriting as it verifies property ownership and loan details, ensuring accurate risk assessment and policy issuance. Underwriters use this statement to confirm the property's address, outstanding loan amount, and lender information, which directly impact flood insurance requirements and premiums. |

| 12 | Loss History Report (CLUE Report) | A Loss History Report (CLUE Report) is essential for flood insurance underwriting as it provides detailed information on prior claims related to water damage or flooding, helping insurers assess risk accurately. This report enables underwriters to identify patterns of property loss, improving the precision of flood insurance eligibility and premium calculations. |

| 13 | Property Tax Assessment | Property tax assessment documents provide critical information about the property's value and characteristics, which insurers use to evaluate flood insurance risk accurately. These assessments help underwriters verify property details such as size, construction type, and location relative to flood zones, ensuring precise premium calculation. |

| 14 | Building Plans or Blueprints | Building plans or blueprints are essential documents for flood insurance underwriting, providing detailed information about the property's structure, foundation, and elevation relative to flood risk areas. Accurate architectural drawings enable underwriters to assess potential flood damage, determine appropriate coverage levels, and calculate premium rates based on construction materials and flood defenses. |

| 15 | Occupancy Certificate | An Occupancy Certificate is a crucial document for flood insurance underwriting, verifying that a building complies with local building codes and is deemed safe for occupancy, which directly impacts risk assessment. Insurers require this certificate to confirm the property's legal status and ensure that flood risk evaluations are based on authorized and habitable structures. |

| 16 | Construction Date Proof | Proof of construction date, such as building permits, original blueprints, or official tax records, is essential for flood insurance underwriting to assess risk accurately. Lenders and insurers use this documentation to determine compliance with floodplain management regulations and eligibility for specific policy rates. |

| 17 | Location Map or Site Plan | A detailed location map or site plan is essential for flood insurance underwriting, as it precisely identifies the property's proximity to flood zones and water bodies. This documentation helps assess flood risk and determines the appropriate premium rates based on elevation and local floodplain data. |

| 18 | Flood Mitigation Improvements Documentation | Flood insurance underwriting requires detailed documentation of flood mitigation improvements such as elevation certificates, proof of installation of sump pumps or backflow valves, and records of property modifications to reduce flood risk. These documents help underwriters assess risk accurately and potentially lower premiums by demonstrating enhanced flood resistance measures. |

| 19 | Contact Information Sheet | A Contact Information Sheet for flood insurance underwriting typically includes the policyholder's full name, phone number, email address, and mailing address to ensure accurate communication. Insurance underwriters use this data to verify identity, assess risk factors, and facilitate precise documentation throughout the flood insurance application process. |

| 20 | Utility Bills (for address verification) | Utility bills serve as critical documentation in flood insurance underwriting by providing verifiable proof of the insured property's address, ensuring accurate risk assessment based on location-specific flood zone data. Common acceptable utility bills include water, electricity, gas, or landline phone statements dated within the past 30 to 60 days, which validate the property's occupancy and help underwriters confirm eligibility for flood insurance coverage. |

Introduction to Flood Insurance Underwriting

Flood insurance underwriting involves assessing the risk of flood damage to a property before issuing a policy. This process requires specific documents to evaluate the property's location, structure, and flood history. Understanding these requirements is essential for securing appropriate flood insurance coverage.

Key Documentation Required for Flood Insurance

What documents are needed for flood insurance underwriting? Flood insurance underwriting requires specific documentation to assess the risk accurately. Key documents include the property deed, flood zone determination, and elevation certificate.

Why is an elevation certificate important for flood insurance? The elevation certificate provides detailed information about a property's elevation relative to the base flood elevation, helping underwriters evaluate flood risk. This document is essential for determining premium rates and eligibility.

Which property details are necessary during flood insurance underwriting? Property details such as the construction type, age, and foundation characteristics are crucial. These details help underwriters understand the vulnerability of the property to flood damage.

How does flood zone determination affect the underwriting process? Flood zone determination identifies whether a property lies within a high-risk flood area. This information guides the insurance provider in setting appropriate coverage levels and premiums.

What proof of ownership is required for flood insurance? A clear copy of the property deed or mortgage documentation confirms ownership. This proof ensures the applicant has a legitimate interest in securing flood insurance for the property.

Property Risk Assessment and Verification

Flood insurance underwriting requires precise documentation to evaluate property risk and verify eligibility. Proper assessment ensures accurate premium calculation and policy issuance.

- Flood Zone Determination - A flood zone map or elevation certificate to identify the property's flood risk level.

- Property Elevation Data - Elevation certificates or surveys that indicate the building's height relative to the Base Flood Elevation (BFE).

- Building and Site Information - Detailed property descriptions including age, construction materials, and flood vents for risk verification.

Importance of Accurate Elevation Certificates

Flood insurance underwriting requires specific documents to accurately assess risk. Key among these is an elevation certificate, which details the property's height relative to base flood levels.

Accurate elevation certificates are essential because they directly influence premium rates and coverage eligibility. Incorrect or outdated certificates can lead to increased costs or denial of coverage. Providing precise elevation information ensures your flood insurance reflects the true risk, protecting both property and finances effectively.

Verifying Ownership and Property Details

| Document Type | Purpose | Details Required |

|---|---|---|

| Property Deed | Verifying Ownership | Owner's name, property address, legal description |

| Title Report | Confirming Ownership and Liens | Ownership status, encumbrances, restrictions |

| Mortgage Statement | Ownership Verification | Current mortgage holder, loan amount, property address |

| Property Tax Records | Verify Ownership and Property Valuation | Owner's name, assessed value, tax identification number |

| Survey or Site Plan | Validate Property Boundaries and Flood Zone | Property dimensions, location, flood zone classification |

| Building Permit or Construction Documents | Verify Property Characteristics and Compliance | Construction date, building type, elevation details |

| Flood Zone Determination Letter | Confirm Flood Risk and Property Location | FEMA flood zone designation, map panels, date issued |

Flood Zone Determination and Mapping

Flood insurance underwriting requires accurate flood zone determination to assess risk levels. Flood zone maps issued by the Federal Emergency Management Agency (FEMA) serve as the primary reference for identifying flood-prone areas.

Your property's location in relation to these flood zones must be validated with official Flood Insurance Rate Maps (FIRMs). These maps provide detailed information about flood hazards, which underwriters use to set premiums and coverage limits.

Evaluating Previous Flood Loss History

Flood insurance underwriting requires a thorough evaluation of previous flood loss history to assess risk accurately. Documentation such as past flood claims, loss adjustment reports, and proof of repairs are essential for this process.

Providing detailed records of prior flood damage helps underwriters determine coverage eligibility and premium rates. You should gather all relevant documents that demonstrate the extent and frequency of previous flood incidents on the property.

Compliance with Local and Federal Regulations

Flood insurance underwriting requires strict compliance with local and federal regulations to ensure proper risk assessment. Accurate documentation helps meet these legal standards and secures coverage eligibility.

- Flood Zone Determination - A FEMA Flood Insurance Rate Map (FIRM) or equivalent local flood zone report is necessary to verify the property's flood risk classification under federal guidelines.

- Elevation Certificate - This document provides the building's elevation relative to the base flood elevation, ensuring adherence to National Flood Insurance Program (NFIP) requirements.

- Proof of Property Ownership - Legal documentation such as a deed or tax records confirms ownership and the insurable interest required by underwriting regulations.

Underwriting Review and Decision-Making Process

Flood insurance underwriting requires detailed documentation to assess risk accurately. Key documents include your property's elevation certificate, flood zone determination, and prior flood loss history. These documents enable underwriters to evaluate exposure, establish premiums, and make informed coverage decisions effectively.

What Documents are Needed for Flood Insurance Underwriting? Infographic