To buy a house with an FHA loan, you need key documents including proof of income such as pay stubs and tax returns, employment verification, and a valid government-issued ID. Lenders also require bank statements to verify assets and a credit report to assess financial responsibility. These documents ensure compliance with FHA guidelines and help streamline the loan approval process.

What Documents are Needed to Buy a House with an FHA Loan?

| Number | Name | Description |

|---|---|---|

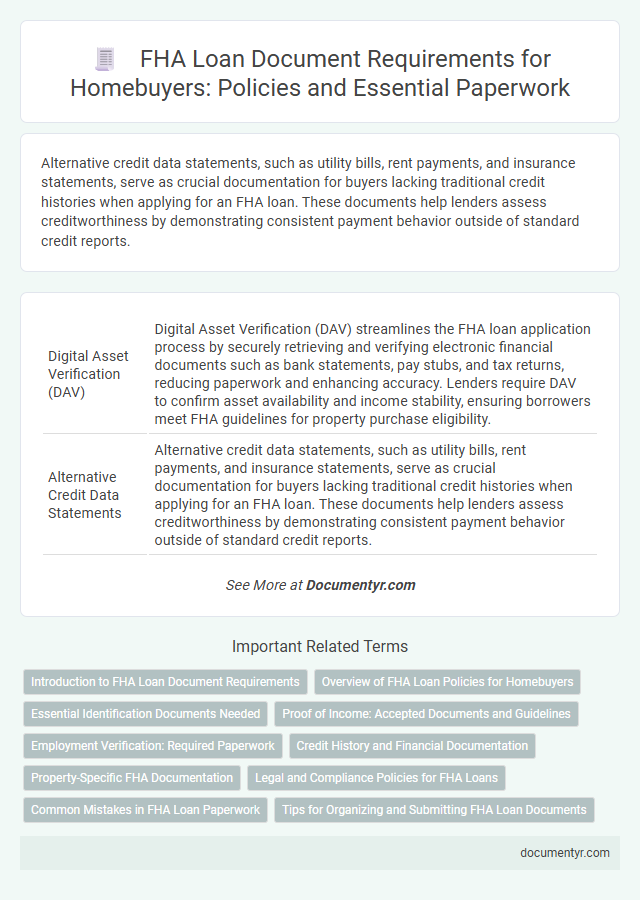

| 1 | Digital Asset Verification (DAV) | Digital Asset Verification (DAV) streamlines the FHA loan application process by securely retrieving and verifying electronic financial documents such as bank statements, pay stubs, and tax returns, reducing paperwork and enhancing accuracy. Lenders require DAV to confirm asset availability and income stability, ensuring borrowers meet FHA guidelines for property purchase eligibility. |

| 2 | Alternative Credit Data Statements | Alternative credit data statements, such as utility bills, rent payments, and insurance statements, serve as crucial documentation for buyers lacking traditional credit histories when applying for an FHA loan. These documents help lenders assess creditworthiness by demonstrating consistent payment behavior outside of standard credit reports. |

| 3 | Electronic Consent Forms (eConsent) | Electronic Consent Forms (eConsent) are essential documents when applying for an FHA loan, allowing lenders to obtain your permission to collect and verify personal and financial information electronically. These electronically signed forms expedite the approval process by ensuring compliance with the Electronic Signatures in Global and National Commerce (ESIGN) Act and the Uniform Electronic Transactions Act (UETA). |

| 4 | Automated Employment Verification Reports | Automated Employment Verification Reports provide lenders with real-time data confirming the borrower's employment status and income consistency, which is crucial for FHA loan approval. These reports streamline the documentation process by reducing the need for manual employment verification, ensuring faster and more accurate eligibility assessments for homebuyers. |

| 5 | Gift Fund Source Traceability Documents | Lenders require gift fund source traceability documents to verify the legitimate origin of funds used for the down payment in an FHA loan, which typically include a gift letter, bank statements from the donor, and a paper trail showing the transfer of funds. These documents ensure compliance with FHA guidelines by confirming the donor's financial ability and that the gift is non-repayable. |

| 6 | Personalized Credit Explanation Letters | Personalized Credit Explanation Letters are essential documents for an FHA loan application, providing detailed reasons for any past credit issues such as late payments, bankruptcies, or collections. These letters help lenders assess the borrower's creditworthiness beyond credit scores, increasing the chances of loan approval by clarifying unique financial circumstances. |

| 7 | Cryptocurrency-to-Cash Fund Source Statements | Cryptocurrency-to-cash fund source statements must include transaction histories, wallet addresses, and verification of conversion dates to comply with FHA loan requirements for transparency and anti-money laundering policies. Lenders require detailed documentation proving the cryptocurrency funds have been legally converted to cash and traced through banking statements before approving the loan. |

| 8 | Rent Payment Ledger via Fintech Apps | To buy a house with an FHA loan, a detailed rent payment ledger from fintech apps can serve as proof of consistent rental history, demonstrating the borrower's reliability and financial stability. These digital payment records, often linked to bank statements, simplify verification of on-time rent payments required by lenders to assess creditworthiness under FHA guidelines. |

| 9 | Social Security Verification API Outputs | To buy a house with an FHA loan, Social Security Verification API outputs must confirm the borrower's valid Social Security Number and eligibility status, ensuring compliance with federal lending guidelines. This verification process typically requires submission of government-issued identification and Social Security card details to validate identity before loan approval. |

| 10 | Environmental Hazard Disclosure Addendums | Environmental Hazard Disclosure Addendums are critical documents required when purchasing a house with an FHA loan, as they inform borrowers about potential risks such as lead-based paint, asbestos, radon, or mold presence. Lenders mandate these disclosures to ensure compliance with federal regulations and protect homeowners from unknowingly buying properties with environmental liabilities. |

Introduction to FHA Loan Document Requirements

When purchasing a home with an FHA loan, specific documents are essential to verify eligibility and streamline the approval process. These documents demonstrate financial stability and meet the Federal Housing Administration's guidelines.

Key documents include proof of income such as pay stubs, tax returns, and W-2 forms to assess your ability to repay the loan. Lenders also require a credit report and bank statements to evaluate your financial health. Additionally, identification documents and the purchase agreement for the property are necessary to complete the application.

Overview of FHA Loan Policies for Homebuyers

What documents are needed to buy a house with an FHA loan? Homebuyers must prepare key financial paperwork to comply with FHA loan requirements. These documents help verify income, creditworthiness, and eligibility under FHA policies.

Essential Identification Documents Needed

Buying a house with an FHA loan requires specific identification documents to verify your eligibility and identity. Providing the correct paperwork ensures a smooth approval process and compliance with FHA guidelines.

- Valid Government-Issued ID - A driver's license or passport is required to confirm your identity and residency status.

- Social Security Number - Essential for credit checks and verifying your financial history with the FHA loan program.

- Proof of Employment and Income - Recent pay stubs and W-2 forms help lenders assess your ability to repay the loan.

Proof of Income: Accepted Documents and Guidelines

Proof of income is a critical requirement when applying for an FHA loan to buy a house. Your submitted documents must clearly verify your financial stability and ability to repay the mortgage.

- Recent Pay Stubs - Provide your last 30 days of pay stubs to show current employment income.

- W-2 Forms - Submit W-2 forms from the past two years to demonstrate consistent earnings.

- Tax Returns - Include signed federal tax returns for the previous two years to verify total income and identify self-employment income when applicable.

Employment Verification: Required Paperwork

Employment verification is a critical component when applying for an FHA loan to buy a house. Lenders typically require recent pay stubs, W-2 forms from the past two years, and employer contact information to confirm steady income. Providing these documents ensures the borrower meets the FHA's income stability requirements for loan approval.

Credit History and Financial Documentation

| Document Type | Description | Importance for FHA Loan |

|---|---|---|

| Credit Report | Official credit report from all major credit bureaus. This report includes your credit score, payment history, outstanding debts, and credit inquiries. | Required to assess creditworthiness. FHA loans typically require a minimum credit score of 580 for maximum financing. |

| Credit Explanation Letter | If there are any credit issues such as late payments or collections, a letter explaining the reasons behind them can be submitted. | Helps lenders understand special circumstances that affected your credit history. |

| Income Verification | Documents such as recent pay stubs, W-2 forms, and tax returns from the past two years. | Confirms consistent income to ensure loan repayment ability. |

| Employment History | Proof of stable employment over the past two years, including employer contact information. | Demonstrates financial stability required by FHA underwriting guidelines. |

| Bank Statements | Recent statements showing savings, checking account balances, and any large deposits or withdrawals. | Provides insight into available funds for down payment, closing costs, and reserves. |

| Debt Information | Details on current debts such as student loans, car loans, credit cards, and other financial obligations. | Used to calculate Debt-to-Income (DTI) ratio critical for FHA loan eligibility. |

Property-Specific FHA Documentation

When purchasing a house with an FHA loan, certain property-specific documents are essential to ensure eligibility and compliance. These documents verify the condition and value of the property to meet FHA standards.

Your lender requires an FHA appraisal report that includes a detailed inspection of the home's condition and any required repairs. Additionally, the property must have a valid certificate of occupancy or proof that the home meets local building codes.

Legal and Compliance Policies for FHA Loans

To buy a house with an FHA loan, borrowers must provide a valid government-issued photo ID, proof of income such as pay stubs or tax returns, and a complete credit history report. Legal and compliance policies require submission of the FHA appraisal report to ensure the property meets minimum standards. Additionally, borrowers must furnish the signed loan application and evidence of employment to comply with FHA regulations and underwriting guidelines.

Common Mistakes in FHA Loan Paperwork

Buying a house with an FHA loan requires specific documentation to ensure the loan process goes smoothly. Common mistakes in FHA loan paperwork often delay approvals and complicate the home buying experience.

- Incomplete Income Verification - Submitting partial or outdated pay stubs and tax returns can lead to loan processing delays.

- Missing Employment History - Failure to provide a consistent two-year employment record can result in application rejection.

- Insufficient Credit Documentation - Not including all required credit reports and explanations for discrepancies may cause underwriting issues.

Thoroughly prepared and accurate FHA loan documents help prevent common errors and expedite home buying approval.

What Documents are Needed to Buy a House with an FHA Loan? Infographic